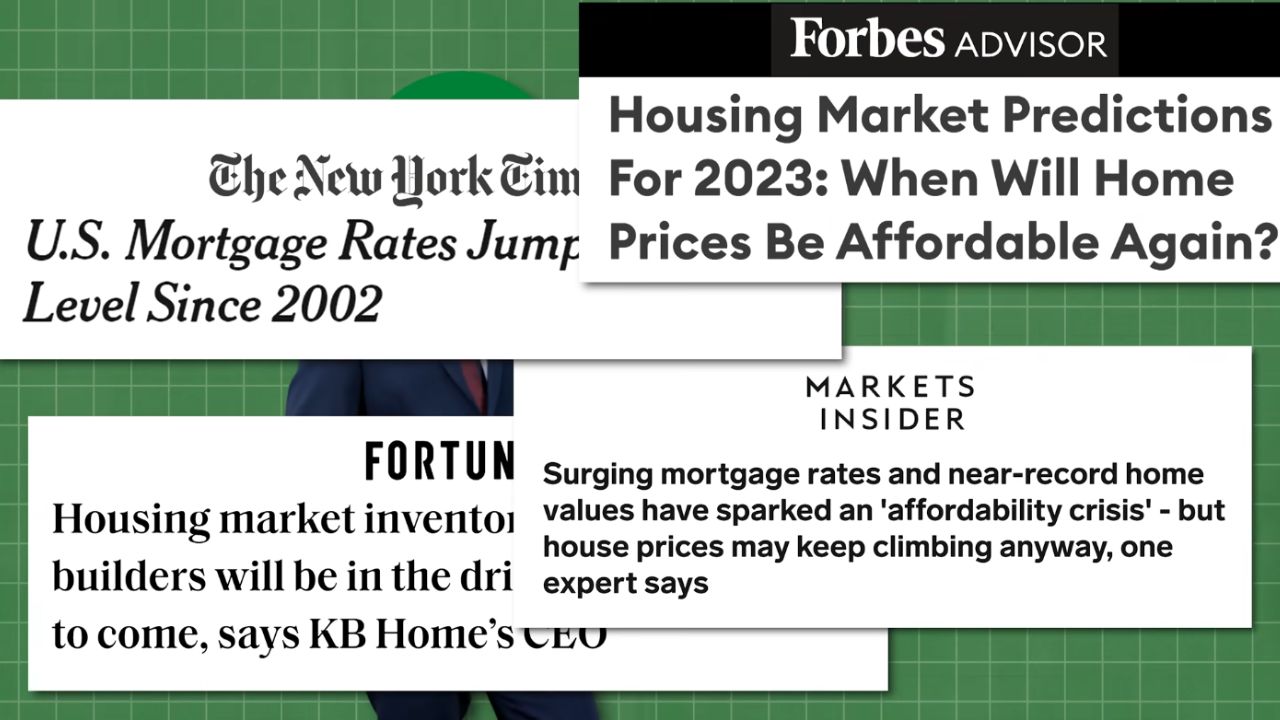

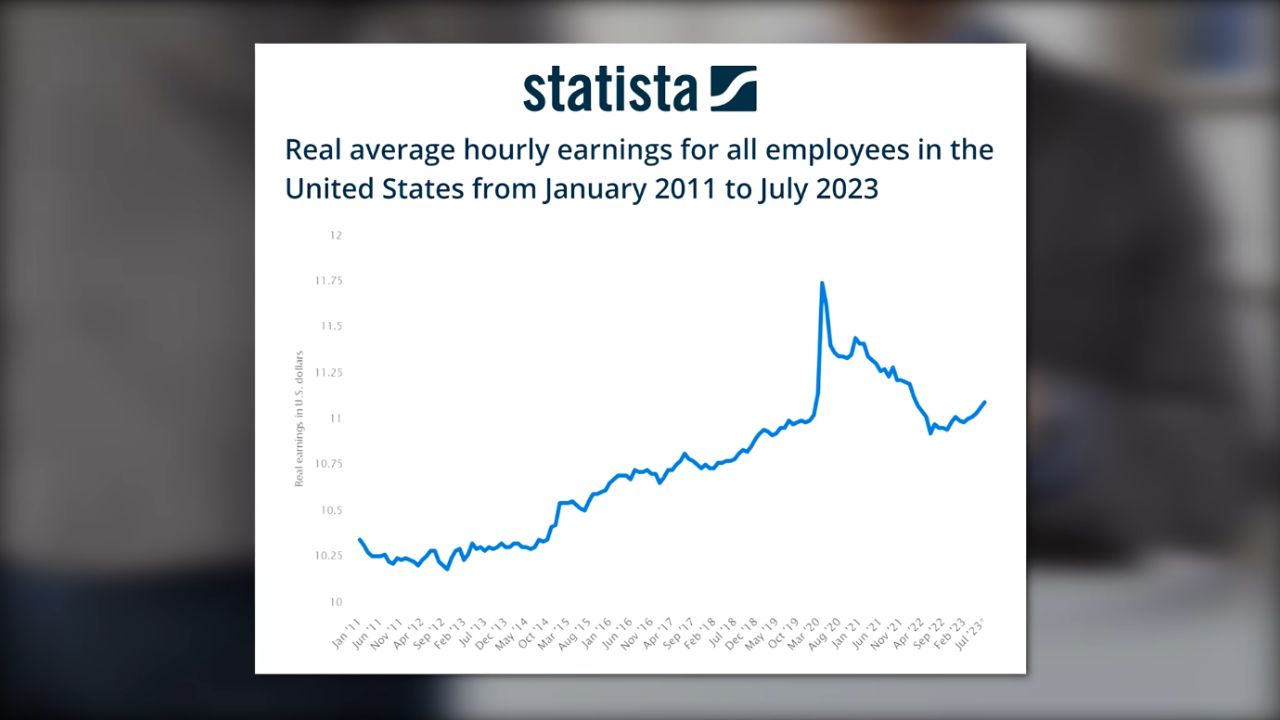

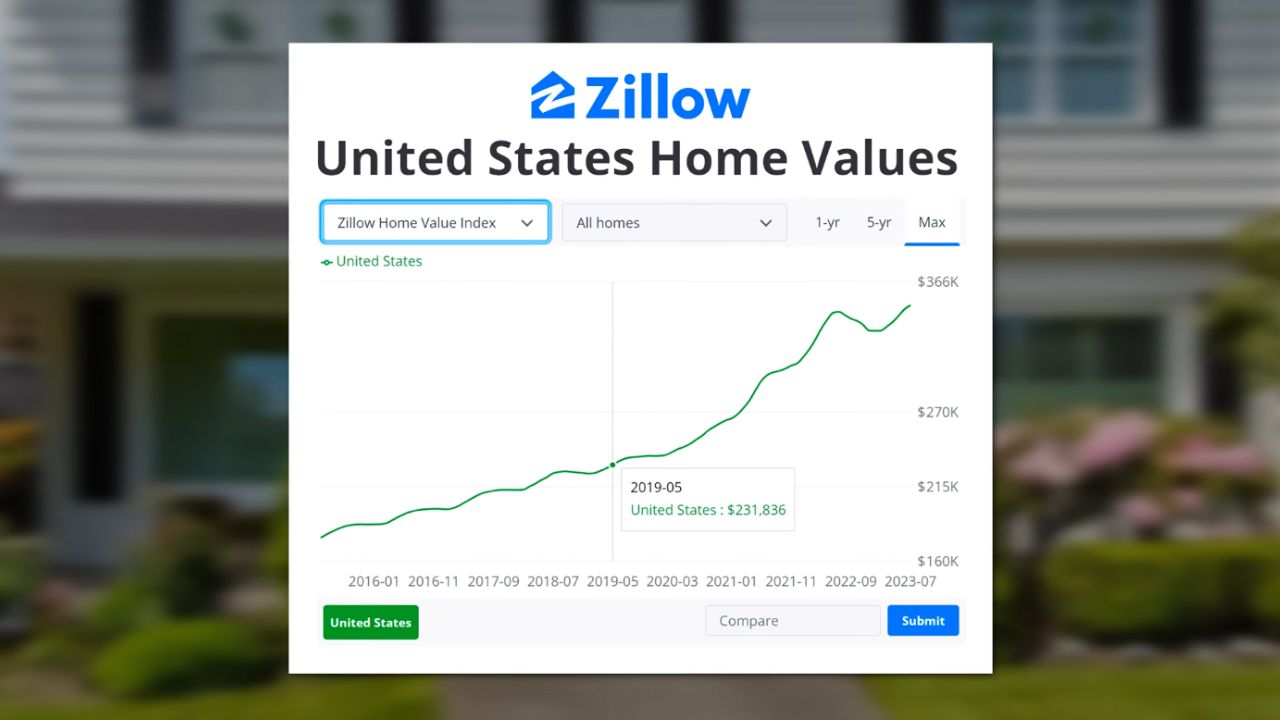

In recent years, the dream of homeownership has become increasingly elusive for many Americans, particularly young adults. With soaring home prices outpacing wage growth, the prospect of saving for a down payment seems daunting, if not impossible. Despite this, the housing market continues to thrive, leaving many to wonder: if nobody can afford to buy a house, who’s driving the demand?

The Paradox of Rising Home Prices

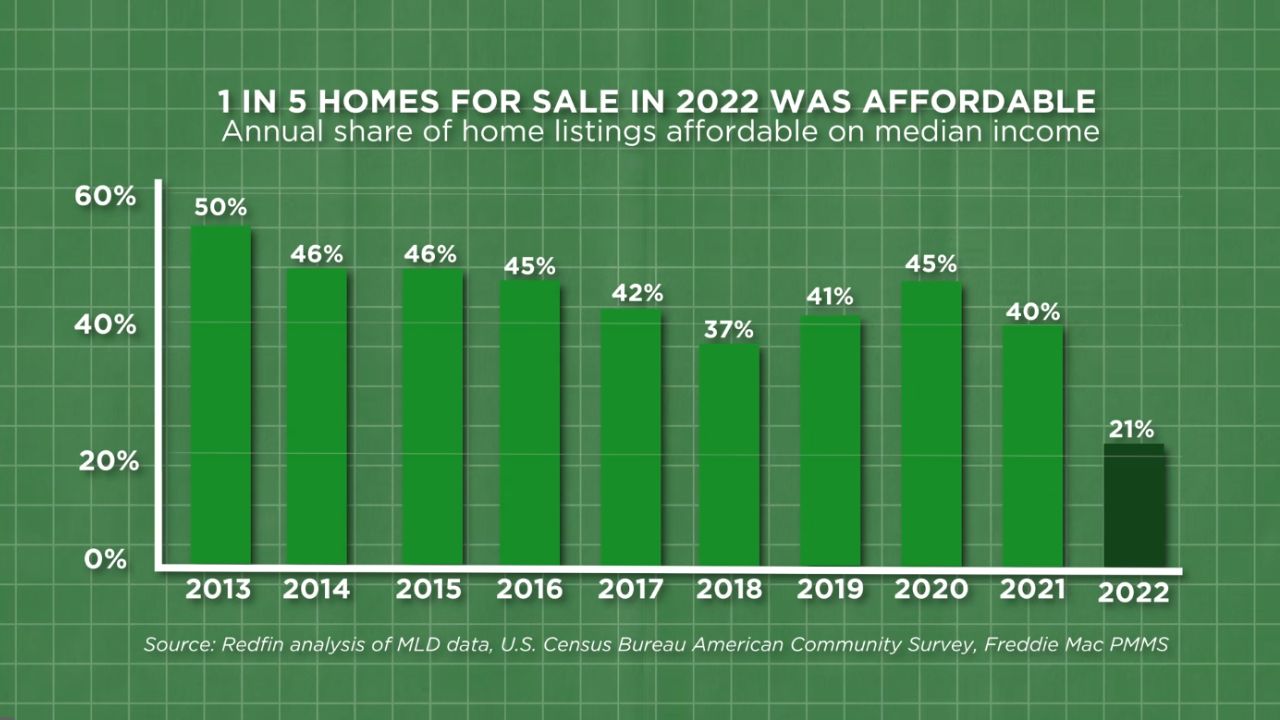

The paradox of rising home prices amidst declining affordability seems counterintuitive. How can homes continue to appreciate in value when a significant portion of the population can’t afford them? The answer lies in a complex interplay of market dynamics and financial mechanisms that perpetuate the cycle of rising prices.

The Role of Down Payments

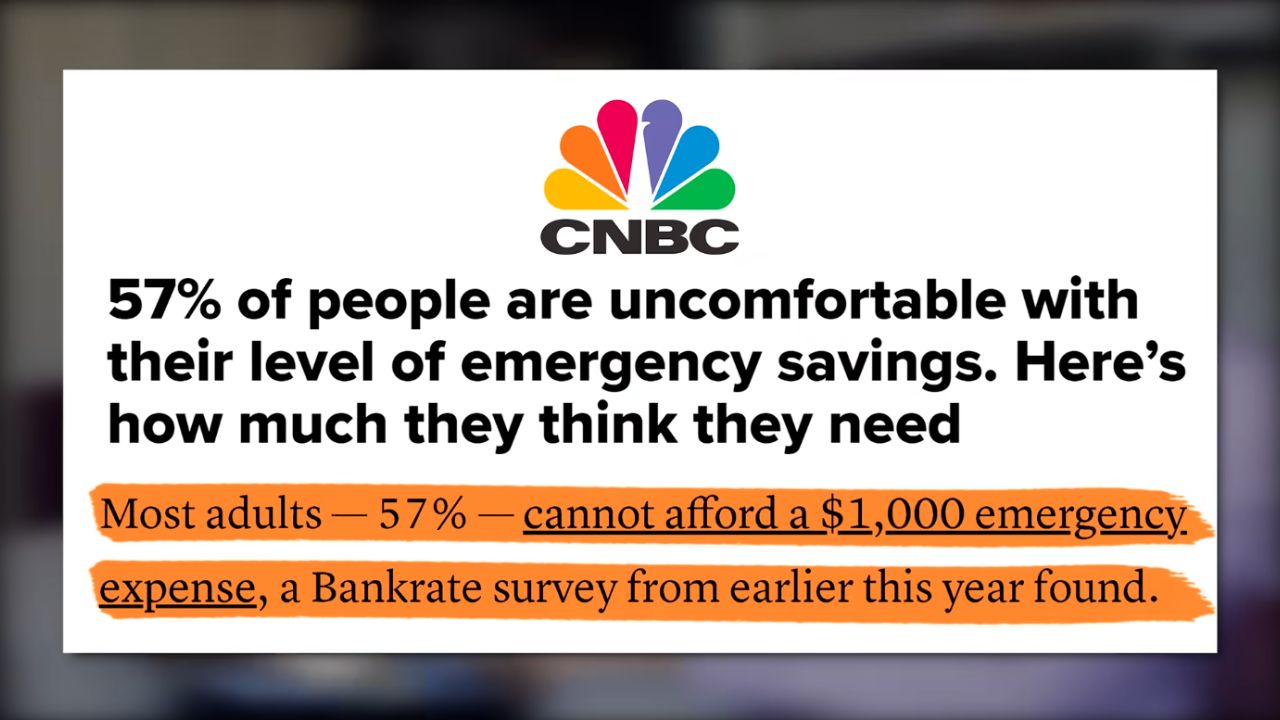

Traditionally, saving for a down payment has been a significant barrier to entry into the housing market. However, as home prices escalate, the gap between savings and property values widens, making it increasingly difficult for aspiring homeowners to bridge the divide. While down payments remain a critical factor in purchasing a home, alternative financing options and reduced down payment requirements have enabled more buyers to enter the market.

Financial Innovations and Reduced Entry Barriers

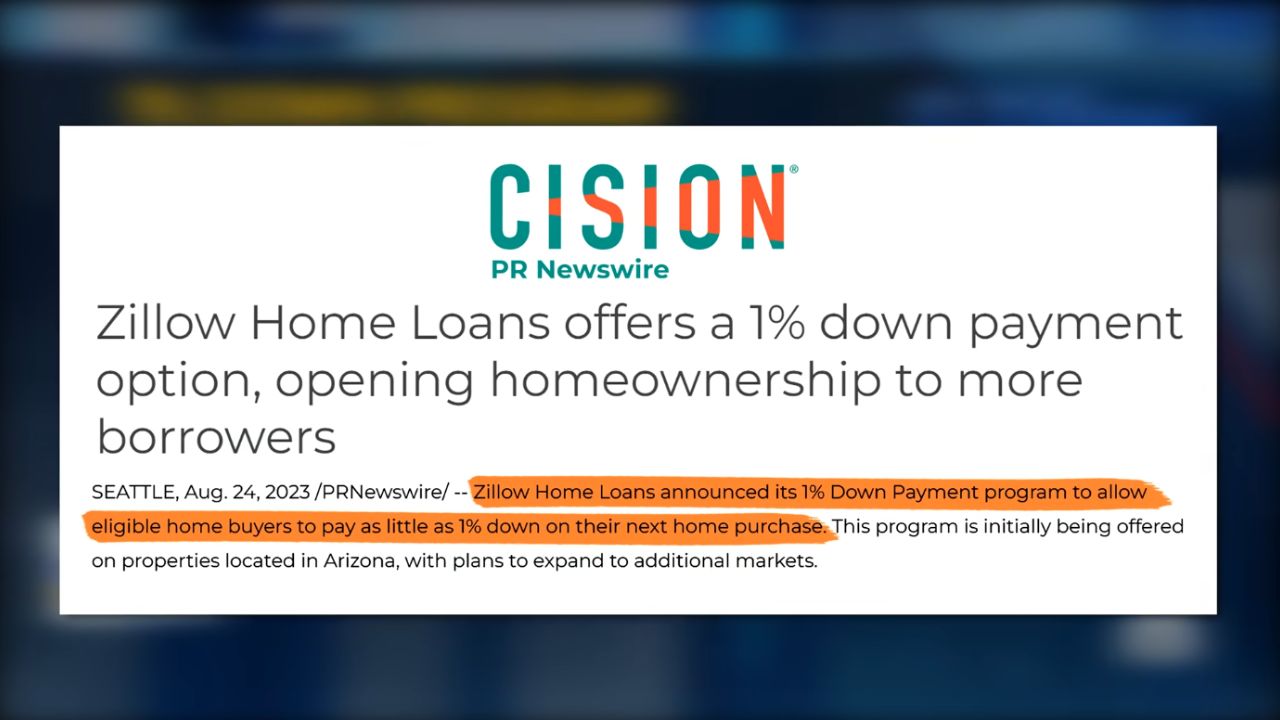

Financial institutions and real estate companies have responded to the affordability crisis with innovative solutions designed to lower the barriers to homeownership. From one percent down payment loans to grant programs that supplement buyer contributions, these initiatives aim to make homeownership accessible to a broader demographic. However, while these measures facilitate entry into the market, they also contribute to inflated prices and heightened demand.

Limited Housing Supply and Reluctant Sellers

Another factor driving the housing market’s resilience is the limited supply of available homes for sale. Despite growing demand, many homeowners are hesitant to sell, citing concerns about finding affordable housing alternatives and navigating the competitive rental market. As a result, inventory levels have dwindled, further fueling competition among buyers and exerting upward pressure on prices.

Demographic Trends and Shifting Preferences

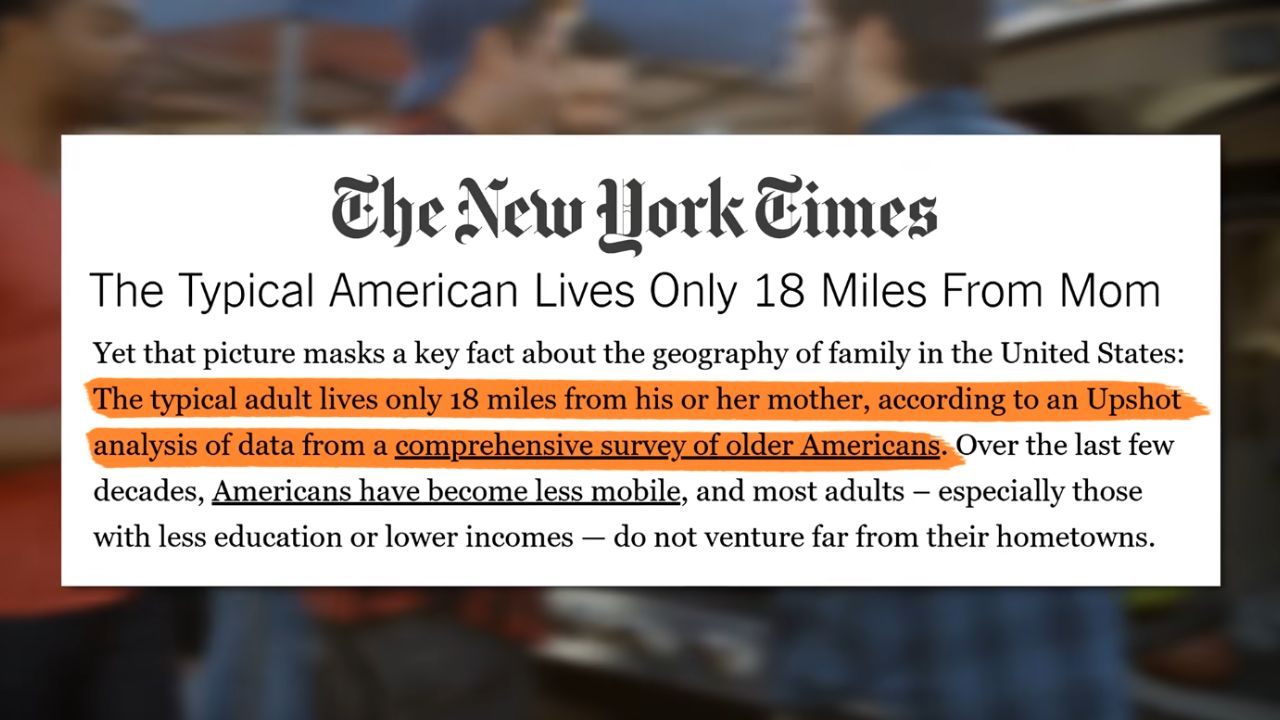

Demographic trends, including an aging population and changing household dynamics, also play a role in shaping housing market dynamics. Longer tenure in existing homes, coupled with a reluctance to downsize or relocate, reduces the supply of available properties and intensifies competition among buyers. Additionally, shifting preferences towards multi-generational living arrangements and remote work have altered housing demand patterns, further complicating the affordability landscape.

Investor Influence and Market Speculation

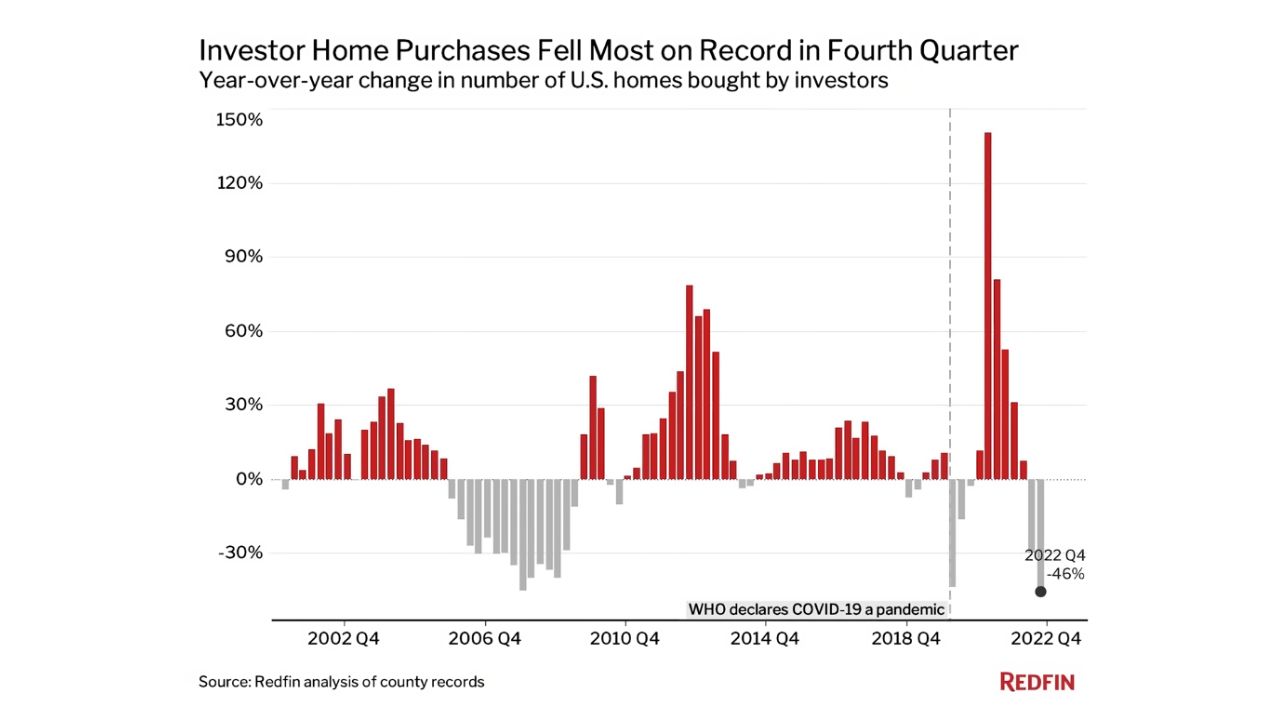

Investors, including institutional buyers and real estate investment trusts (REITs), have emerged as significant players in the housing market, driving demand and influencing pricing trends. With a focus on rental income and capital appreciation, these investors contribute to the commodification of housing and exacerbate affordability challenges for prospective buyers. While their presence adds liquidity to the market, it also perpetuates speculation and volatility.

Potential Market Corrections and Uncertain Futures

Despite the housing market’s resilience, signs of potential correction loom on the horizon. Slowing investor activity, regulatory interventions, and economic uncertainties could disrupt the status quo and trigger adjustments in pricing dynamics. While homeownership remains a cornerstone of the American dream, its attainability hinges on addressing systemic inequities, promoting affordability, and fostering sustainable market practices.

An Unsustainable Trajectory

As the debate over housing affordability intensifies, it’s clear that the current trajectory is unsustainable. Addressing the root causes of the affordability crisis requires a multi-faceted approach, encompassing policy reforms, financial literacy initiatives, and community-driven solutions. It is imperative that we foster inclusivity, promote affordability, and prioritize long-term sustainability, so we can ensure that the dream of homeownership remains within reach for all Americans, regardless of income or background.

Alternative Financing Options

What do you think? How can policymakers and stakeholders collaborate to address the systemic challenges contributing to the housing affordability crisis? What role do alternative financing options and innovative housing models play in expanding access to homeownership for underserved communities?

Demographic Shifts

How can we strike a balance between market-driven dynamics and regulatory interventions to promote affordability and stability in the housing market? What impact do demographic shifts and evolving lifestyle preferences have on housing demand and affordability trends?